Meanwhile, the national vacancy rate ticked up for a third consecutive quarter to reach 5.0%. New industrial projects are leasing quickly and often before construction is complete, with vacancy concentrated in older properties.

“Much of the older-generation industrial space vacated as users have upgraded to newly constructed properties remains unleased,” said Matt Dolly, Research Director in New Jersey. “While that results in what appears to be increased availability at the national level, the scarcity of functional space in prime locations is slowing absorption. Users are committing to lease newer, more efficient properties even before construction has started rather than take an aging alternative in a less desirable location.”

Developers are racing to answer unmet demand and had 427.5 million square feet of construction underway at the end of the quarter. That’s up from 407 million square feet in the second quarter, also a record. The volume of new product entering the market helped raise average asking rent to $6.42 per square foot.

“E-commerce and logistics operations are typically less sensitive to rent than to transportation costs,” Dolly said. “These occupiers are more likely to consider locations that shorten last-mile deliveries and reduce overall operating cost.”

In some built-out markets such as Southern California, developers must vie for sites to introduce new supply, often by acquiring and redeveloping existing structures. Of the 47 industrial markets tracked by Transwestern, the region posted the three lowest vacancy rates in the third quarter with Los Angeles at 1.2%, Orange County at 2.4% and the Inland Empire at 2.8%.

Michael Soto, Research Manager in Southern California, says uncertainty stemming from the ongoing U.S.-China trade war hasn’t dampened that market’s occupier or investor demand for industrial real estate.

“Strong industrial real estate fundamentals in the Greater Los Angeles metro continue to create the most supply-constrained conditions in the country,” Soto said. “Investors have responded with nearly double-digit, year-over-year rental rate growth, record-high pricing, and record-low average cap rates.

Other markets with vacancy below 4% include Detroit (3.3%); Long Island, New York (3.2%); Minneapolis (3.2%); Nashville, Tennessee (3.6%); New Jersey (3.5%); and Raleigh/Durham, North Carolina (3.7%).

Healthy consumer spending continues to support industrial demand and is expected to strengthen in the holiday season, though at a slower rate than in 2018. Transportation and warehousing employment continued to expand in the third quarter, while business confidence slipped, especially in manufacturing.

Houston has, for the most part, survived the oil downturn, but some areas are still in recovery.

Houston has, for the most part, survived the oil downturn, but some areas are still in recovery.

While WeWork’s precipitous drop in valuation, from $47 billion in January 2019 to

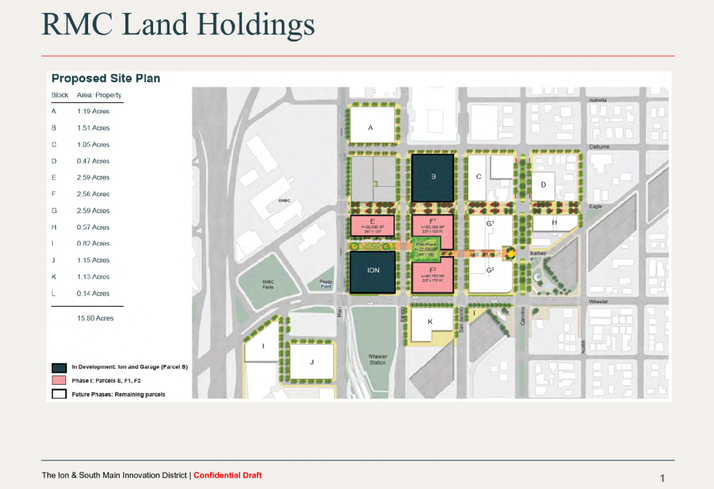

While WeWork’s precipitous drop in valuation, from $47 billion in January 2019 to  People who think Houston is all about urban sprawl haven’t been to Houston lately. Houston’s 610 Loop has been a hotbed for infill development. A stretch of land just south of Buffalo Bayou — roughly 1.5 miles long and 0.5 miles deep — is attracting infill development at a rapid pace. The latest projects, a 600-unit mid-rise with 50K SF of retail from GID and a separate $500M mixed-use development from DC Partners, are a sure sign the city’s real estate perception is changing.

People who think Houston is all about urban sprawl haven’t been to Houston lately. Houston’s 610 Loop has been a hotbed for infill development. A stretch of land just south of Buffalo Bayou — roughly 1.5 miles long and 0.5 miles deep — is attracting infill development at a rapid pace. The latest projects, a 600-unit mid-rise with 50K SF of retail from GID and a separate $500M mixed-use development from DC Partners, are a sure sign the city’s real estate perception is changing.